01 Medicare and Medicaid

Medicare was created in 1965 to guarantee access to healthcare for those over 65 years of age, people with a disability that prevents them from working or people on dialysis (a prohibitively expensive life saving treatment for renal failure). All working individuals pay into the pot for those receiving Medicare (Federal Insurance Contribution Act, FICA).

Define benefits:

- Part A: the government pays the hospital directly for inpatient care

- Part B: the government pays the hospital directly for outpatient care

- Part C: the government pays an insurance company who pays the hospital

- Part D: the government pays for medications and prescriptions

Medicare doesn’t pay for everything. Some patients have out of pocket costs (based on how much people worked before and paid into the system). Those who worked less than 10 years, need to pay something out of pocket for hospitalizations. For Part B, everyone has to pay something (depending on your income). Both Part A and B have deductibles. So some people buy medigap insurance to cover these extra costs.

The cost of Medicare is growing. As the number of older people (ie, people who take money out of the system) increases and the number of people working (ie, those who put money into the system) decreases. Plus medical care is getting more expensive. We are spending more than we are saving. When we can’t cover the costs, we’re said to be insolvent. According to the Center on Budget and Policy Priorities, “The 2019 report of Medicare’s trustees finds that Medicare’s Hospital Insurance (HI) trust fund will remain solvent — that is, able to pay 100 percent of the costs of the hospital insurance coverage that Medicare provides — through 2026.”

02 PPACA Introduction

The ACA for 2010 set out to increase quality, increase the number of people covered by insurance and decrease cost. There are several parts to the ACA:

- Consumer protections: elimination of lifetime limits and discrimination against those with pre-existing conditions

- Individual mandates (people need to have insurance, either from their employer or self-purchased) and employer mandates (companies of 50+ employees need to buy insurance for their workers)

- Medicaid expansion: increases the number of people who qualify for state run Medicaid

- Subsidies given to people and small companies to help them buy insurance through tax credits

- Healthcare Exchanges: state run marketplaces for people to buy insurance

If you have oodles of free time and want to read the actual bill, it’s available here (Affordable Care Act). Previous students liked having access to it. It’s only here for reference for the morbidly curious. Otherwise, move along.

03 Consumer Protections

- Prohibits insurers from denying coverage to people with pre-existing conditions

- Insurance premiums can only vary based on age, smoking status, location where you live, the number of people in your family and the type of coverage (bronze, silver, gold or platinum). Women cannot be charged more than men.

- There are essential health benefits that must be covered by all policies including preventive care and screenings for women. This includes FDA approved contraceptive methods for women.

- No annual or lifetime coverage caps or dropping people when they become ill. Additionally there’s a maximum out of pocket cost for policies, so people won’t get surprised with huge bills. There are four tiers of coverage: bronze, silver, gold and platinum. Out of pocket costs are 60% for bronze, 70% for silver, 80% for gold and 90% for platinum.

04 Mandates

- Essentially, you have to buy insurance unless you have it from your employer, Medicare, Medicaid, parents (till 26 years old) or you are in jail.

- Insurance companies were forced to provide more comprehensive coverage. That’s a lot of extra cost. In exchange, the PPACA offered them a lot more customers to defray that cost.

- Individual Mandate: if you refuse then you have to pay a penalty. It started out at 1% of your taxable income and was to grow to 2.5% of your taxable income. The ability of the government to force its citizens to buy something was challenged in the Supreme Court. It was ruled to be a tax and persevered. Those not subject to the mandate included undocumented immigrants, Medicaid eligible and Medicare citizens, and those whose insurance coverage would be more than 8% of their household income. The Tax Cuts and Jobs Act of 2017 reduced the penalty to $0, essentially nullifying this mandate.

- We had feared a premium death spiral where people fled the ACA opting for the penalty instead.

- Employer Mandate: any company with more than 50 employees needs to buy insurance for all its employees. Companies have several ways to get around this such as hiring only part time employees.

05 Medicaid Expansion and Subsidies

- Current levels of the Federal Poverty Limit from healthcare.gov.

- The subsidies are meant to help those that are too rich to get Medicare but too poor to get their own insurance. Medicaid eligibility was expanded from 100% of the Federal Poverty Level to 133% to insure more of these people.

- Medicaid is paid for by the states, but many states didn’t have the money to cover this extra cost so the federal government said they would subsidize it initially, tapering down over the years.

- Initially the ACA had considered withholding the pre-existing Medicaid Federal subsidies that states get if they didn’t expand Medicaid. However, the Supreme Court ruled that the government couldn’t force states to expand Medicaid by withholding Medicaid money from those who didn’t. So now states that don’t expand Medicaid, still get the money they were already getting. States who did expand Medicaid to 133% FPL get an additional government subsidy.

- The people left in the middle where they can’t afford insurance but are too rich for Medicaid, get a government subsidy.

- The Medicare Part D drug “donut hole” was also filled. The first $2000 of drugs were paid for and the drugs over $6000 were paid for. The cost between $2000 and $6000 wasn’t paid for. So the ACA covered this hole.

06 Healthcare Exchanges

- Prior to the availability of the healthcare exchanges, it was almost impossible to comparison shop for insurance policies because each policy was completely different. They were also not all in one place. It was comparing apples to oranges.

- Now each insurance plan covers all the same things (essential health benefits). Now it’s comparing oranges to oranges.

- There are four different tiers depending on how much is covered

- Bronze = 60%, the patient is responsible for covering 40%.

- Silver = 70%, the patient is responsible for covering 30%.

- Gold = 80%, the patient is responsible for covering 20%.

- Platinum = 90%, the patient is responsible for covering 10%.

- The thought is that competition will cause policies to be less expensive. To allow a lower price, the insurers would have to force physicians to lower costs.

07 Paying for the ACA

- The Congressional Budget Office predicted that we would save $210b.

- Higher Medicare taxes would be imposed on the wealthy.

- Health insurers and device manufacturers would pay a tax.

- Those with expensive fancy Cadillac plans would also pay a tax.

- Elimination of fraud, waste, abuse, medicare advantage and DiSh payments.

08 A Decade Of the ACA

“Essentially, we are getting rid of Obamacare… . Some people would say, essentially, we have gotten rid of it.”

President Trump, April 2018

Obviously this didn’t happen. Though the anniversary of this law may have flown under the radar due to the pandemic, let’s examine what happened with this controversial law in the past ten years since the ACA was signed into law on March 23, 2010. In this time the law has faced its share of challenges. It has faced repeal by over 70 unsuccessful Republican initiatives2. It has been challenged in court several times, with many reaching the highest court in the land.

Timeline

| July 2009 | Representative Pelosi proposes HR 3962, the Affordable Care for America Act (ACHA) |

| August 25, 2009 | Senator Ted Kennedy (MA-D) dies, putting the Democratic supermajority at risk. Kennedy was a champion for universal healthcare. “Every American should be able to get the same treatment that U.S. senators are entitled to. This is the cause of my life.”1 |

| September 24, 2009 | Paul Kirk (MA-D) becomes interim Senator in Massachusetts, reinstating the supermajority |

| November 7, 2009 | House of Representative vote for AHCA: 219 Democrats and 1 Republican vote for, 29 Democrats and 176 Republicans vote against |

| December 14, 2009 | 60 Democrats vote for Max Baucus’s America’s Healthy Future Act, 39 Republicans vote against and 1 Republican abstains |

| January 2010 | Republican Scott Brown (MA-R) wins Ted Kennedy’s seat |

| March 23, 2010 | President Obama signs the Affordable Care Act into law |

| September 23, 2010 | Seniors get $250 to cover the Medicare D prescription coverage gap |

| 2011 | ACA elements are put into effect. Young adults can stay on their parent’s insurance, Women can see their OB-GYN without prior authorization, preventive care must be covered, lifetime limits are removed, annual limit restrictions removed. |

| October 2013 | Health insurance exchanges scheduled to open for the 2014 enrollment period. These plans would go into effect on January 1, 2014. |

| 2014 | Subsidies for premiums for those earning between 138% and 400% of the federal poverty level (FPL) are enacted. |

| 2014 | Fines enacted for those who fail to obtain insurance as per the mandate. These started at $95 and increased to $695 in 2015 (or 2.5% of income, whichever is greater). |

| 2017 | Tax Cuts and Jobs Act reduces the Penalty for not buying insurance to $0, thus invalidating the mandate. This would be the basis of the challenge to the law in California vs. Texas. |

- A Timeline of Kennedy’s Health Care Achievements And Disappointments

- Efforts to Repeal the Affordable Care Act

- History and Timeline of the Affordable Care Act (ACA)

Legal Threats to the ACA

We won’t test you on any of this. You’re not in law school. Just know that there were a lot of attempts to invalidate or hobble the ACA in the past decade.

In 2012, the Supreme Court consolidated two cases together, National Federation of Independent Business (NFIB) vs Sebeius and Florida vs United States Department of Health and Human Services. The plaintiffs held that the law was unconstitutional as Congress doesn’t have the power to mandate the purchase of insurance under the Commerce clause. On June 28, 2012 the Court decided that the legislatively-declared penalty is a tax, a power that Congress does hold. This case also limited the forced expansion of Medicaid. It was now optional for states to expand Medicaid. To this date (Dec 2021) the following states have not adopted expansion: Florida, Georgia, Kansas, Mississippi, North Carolina, South Carolina, Wisconsin and Wyoming.

The Goldwater Institute claimed in Coons vs Geithner that the Independent Payment Advisory Board has the ability to “dictate how much doctors can charge for medical care, how much insurance companies will pay for it and when patients can get access to cutting-edge treatments.” Since this isn’t reviewable by the Courts or Congress this violated the Separation of Powers doctrine (each branch of government should be able to check the others). This was dismissed on December 19, 2012.

In Pruitt vs Sebelius, an Oklahoma lawsuit, the attorney general, Scott Pruitt, challenged the implementation of the ACA after the IRS finalized a rule allowing the IRS to collect penalties from ACA-non-compliant large companies and local governments. The AG claimed this rule was only enforceable in states that enacted state insurance exchanges instead of opting into the Federal health insurance exchange. This was dismissed in August 2013 in a US District Court.

In 2014, Sissel vs US Department of Health and Human Services claimed that the ACA was unconstitutional despite the finding in NFIB vs Sebelius stating that the mandate violated the Origination Clause, which claims a bill for raising revenue must originate in the US House of Representatives. The District Court dismissed the suit On July 29, 2014, stating that the finding in NFIB vs Sebelius holds as the ACA did originate in the House.

In 2014, US House of Representatives vs Price challenged the cost-sharing programs but was ultimately settled in the DC Court of Appeals.

In 2015, King vs Burwell challenged a Treasury regulation in the ACA. It claimed that state subsidies can only be distributed through state-run exchanges and not the IRS. If a state did not set up such an exchange, the subsidies cannot be distributed thus invalidating the law. On June 25, 2015 the Supreme Court decided 6-3 that subsidies can come from healthcare.gov in states that didn’t set up their own exchange.

In 2016, a Federal Judge ruled that the Federal government cannot assist insurance companies with cost-sharing in order to lower premiums for those families with household incomes between 100-250% of the FPL.

In March 2018, after the Tax Cuts and Jobs Act of 2017 invalidated the mandate, California vs Texas claimed that this invalidated Congress’s taxation powers (as described in NFIB vs Sebelius) thus making the entire law void. The Fifth Court of Appeals heard the case and said that the tax could be severed from the rest of the ACA. Both Texas and California countersued each other. In a 7-2 decision on June 17, 2021 the Supreme Court ruled that Texas’s initial challenge didn’t have standing as they hadn’t shown any past or future injury. The ACA stands.

Summary of the past decade

It has been 10 years since one of the most controversial pieces of healthcare The Affordable Care act came to life, the following is a reflection of the accomplishments of the ACA in the past decade.

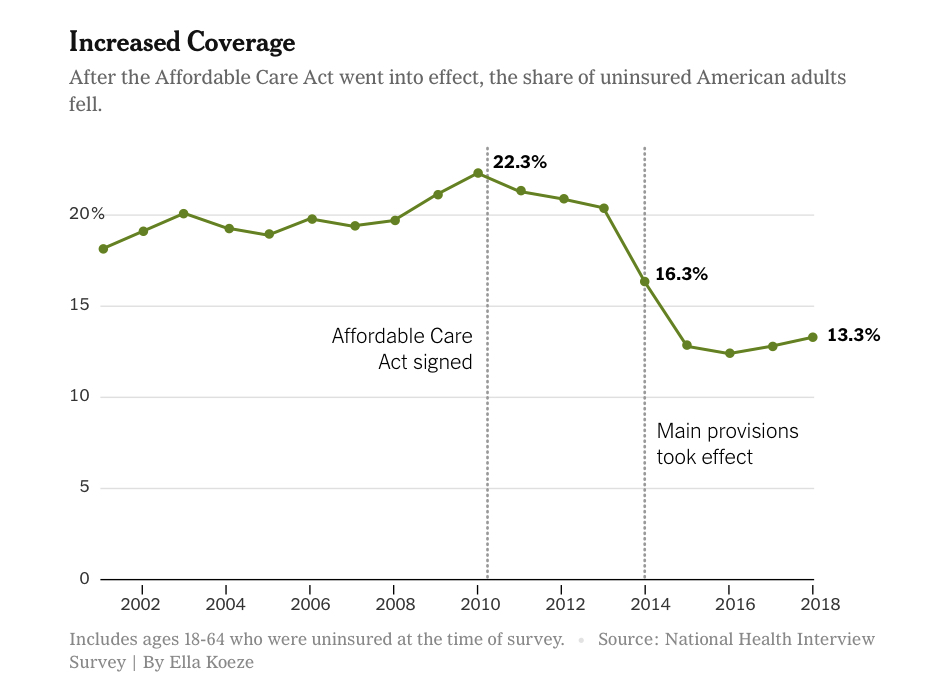

- By 2016 the number of uninsured people decreased to historically low levels, reports estimate that the number dropped to 28.6 million, however it has since increased to 30.4 million.

- To date 36 states and Washington, D.C. under ACA have expanded Medicaid helping millions of lower income individuals. The National Financial Capability Study found that Medicaid expansion led to improvements in some financial outcomes for low-income Americans

- Women can no longer be charged more for insurance, services related to women’s health are also guaranteed

- ACA continues to protect people with pre-existing conditions

- Implementation of the law has been deeply affected by partisan conflict

- Medicare expenditure was almost 20% lower than projected in part because ACA reduced annual increases in payments to hospitals and to Medicare Advantage plans

- Growth of insured people has been associated to increase access to care and greater use of health services

- Some of the ACA coverage gains have been reversed but failure of the congress to repeal the ACA in 2017 led to many of its key components to remain intact such as Medicaid expansion, marketplace subsidies and market reformed. These three components have been some of the most controversial aspects of the reform:

Number of insured

There were 48.6 million uninsured Americans in 2010. The Congressional Budget Office (CBO) predicted that this number would fall to 23 million in 2019 due to the ACA. They revised their estimate to 29 million after the various legal threats to the law. In 2016, there were 28.6 million uninsured in the US and 30.4 million in 2020.

Medicaid expansion

The ACA called for expansion of Medicaid eligibility, through a system of penalties and incentives, requiring all states to cover residents with income below 138% of the federal poverty level. The incentive was simple: the federal government covers 100% of the cost for the first 3 years down to 90% in 2020. Keep in mind, the Federal government covers on average 61% of the cost for the traditional Medicaid population.

The penalty for states that did not comply with Medicare expansion was loss of Federal Medicaid funds for their entire population. The Supreme Court ruled in 2012 that the ACA couldn’t force states to participate in Medicaid expansion. The expansion was optional for each state.

While 36 states and DC have expanded Medicaid (insuring 12.7 million more people), 14 states with Republican leadership chose not to expand Medicaid. This has one important implication. People who earned between 100% and 138% of the FPL and would have been covered had Medicaid been expanded were made ineligible for federal assistance for health insurance. This left a significant number of residents uninsured.

In 2020 due to some pressure from constituents Idaho, Nebraska and Utah expanded Medicaid. Oklahoma and Missouri joined the expansion in 2021.

- In the years since the law has been passed, Medicaid expansion has exceeded expectations with over 12 million more enrollees.

- It is estimated that 2.5 million people are in the Medicaid gap in non-expansion states.

Marketplace Subsidies

| Household Income | <100% FPL | 100-138% FPL | 139-400% FPL | > 400% FPL |

| Under Medicaid Expansion | Gets Medicaid | Gets Medicaid | Receives Subsidies | No subsidies (hopefully employer pays) |

| In States that refused Medicaid Expansion | Gets Medicaid | No coverage | No coverage | No subsidies (hopefully employer pays) |

| Cost-Sharing (overturned in 2016) | 100-250% FPL: Insurers get Federal help keeping premiums low | 100-250% FPL: Insurers get Federal help keeping premiums low |

Prior to the ACA, many individuals and families found it challenging to obtain health coverage. Insurers often declined to cover people with pre-existing health conditions. Premiums were too high which was an even bigger disadvantage for those who were already ill. The ACA addressed these problems by eliminating denials based on pre-existing conditions and subsidizing the purchase of individual insurance through the marketplace. The idea was that premium subsidies ensured that buyers spend no more than a fixed percentage of their income.

The ACA also stipulated that the Federal government would subsidize private insurers to provide cost sharing assistance for people with income 100-250% federal poverty level. These cost sharing provisions have been subject to litigation and in 2016 a federal judge ruled that the government could not help plans with the cost of providing assistance with cost sharing, yet under the new ruling insurers were still obliged to offer a more generous coverage.

- Their average monthly premium was $574, for an $80 savings, though the average enrollee owed less after subsidies ($81).

- For those in the 100-138% FPL range, the average deductible went from $4,375 to $239.

- Dependent coverage for those 19-25 years old went from 34% (in 2010) to 26.5% (in 2013) and later down to 15% (2017). 2.3 million young Americans gained coverage.

- The elimination of the mandate is estimated to have added 1 million Americans (2018) to the uninsured and another 7 million over the next decade.

- Premiums may not have gotten cheaper (the Cato Institute claims they actually doubled), however they are offset by subsidies.

- A Commonwealth Fund survey showed form 2010 to 2018, the number of elderly who couldn’t pay a medical bill fell 17%, those who avoided seeing a doctor dropped 19% and those who skipped a test or treatment dropped 24%.

Markets reformed

As mentioned above one of the major changes brought by ACA was eliminating discrimination against people with pre-existing conditions. The ACA required all insurers to accept all applicants (guaranteed issue) and to renew coverage (guaranteed renewal) for all wishing to do so. Under ACA legislation, insurers were no longer able to charge higher premiums for people with health conditions. Premiums could only be indexed on age, family size, geographic location and smoking status.

The Cato Institute, a Libertarian group, feel that the ACA’s “original sin” was trying to cover those with pre-existing conditions at a price less than what it actually costs to care for them. They had predicted a premium death spiral which never materialized. Some Democrats feel the law diminishes the push for a public option.

The ACA has been under attack since its origin, of all its components the one that has been the most contested is the individual mandate requiring that all Americans have or purchase health insurance otherwise they will have to pay a penalty. In 2012 the Supreme Court upheld the constitutionality of the mandate but in 2017 it was successfully repealed by a Republican Congress which eliminated financial penalties associated with failing to comply with the mandate, the appeal took effect in 2019.

ACA also led to creation of marketplaces or exchanges where different insurers list their policies and buyers can easily compare benefits and premiums. The government has its own platform which is http://www.healthcare.gov but each state has the option to build its own marketplace.

It is estimated that almost half of the coverage has resulted from enrollment through ACA marketplace, the reason is because premium subsidies are being offered. In 2019 for example 87% of the people who purchased insurance received federal assistance.

- Marketplaces enrolled 10.6 million Americans and 87% of them received some sort of assistance.

- While there are still some plans that don’t provide guaranteed issue due to pre-existing condition limitations, it is expected these will slowly dwindle away as there is no Federal assistance to enroll in these plans.

- Lowered costs of prescription meds to seniors by closing the Medicare D donut hole saving seniors $20 billion on drugs.

Other changes to ACA

The Trump administration lifted restrictions on health plans that did not comply with ACA, some of these non-ACA compliant plans include policies that people can purchase to fill a short-term coverage gap. Premium subsidies cannot be used to purchase these types of plans which has led to a lower than expected growth of its market.

Under the Trump administration some states were able to allow work requirements for people to enroll in Medicaid, In Arkansas for example by December of 2018, 17,000 people lost coverage. Most of the affected people were unaware of the need to inform Medicaid of employment status. A federal judge halted the program as there was concern about its effect on coverage.

Healthcare outcomes

The main question that we all ask is what are the ACA effects on the health of the people of the United States? Data is mixed. In 2019 JAMA published and article which found that Medicaid expansion was associated with reduction in mortality from cardiovascular disease and mortality from end stage renal disease.

- Utilization of primary care and specialty care, prescription drugs have increased among low-income adults comparing Medicaid-expansion states to non-expansion states.

- There is increased utilization of services for mental health and substance use.

- The National Bureau of Economic Research estimates that the failure to expand Medicare in certain states may have led to 15,600 avoidable deaths between 2014-2017.

Costs

Did this make things cheaper? Depends who you ask.

- In 2019, the Federal government spent $128 billion dollars on healthcare expenditures. This is less than the $172 billion the CBO had predicted. This decrease may have been due to decreased growth in healthcare costs, though.

- Over the next 10 years, the ACA is predicted to cost $1.7 trillion dollars.

- For comparison, the Federal government takes in about $4.17 trillion dollars per year in revenue. States take in about $2.26 trillion.

- There are decreased out of pocket costs among enrolled people leading to better financial well-being and reports of less people having trouble paying bills.

- Leftover money from premium payments is limited to 20% for insurers (medical loss ratio). The rest must be returned to the insured, which amounted to $1.37 billion.

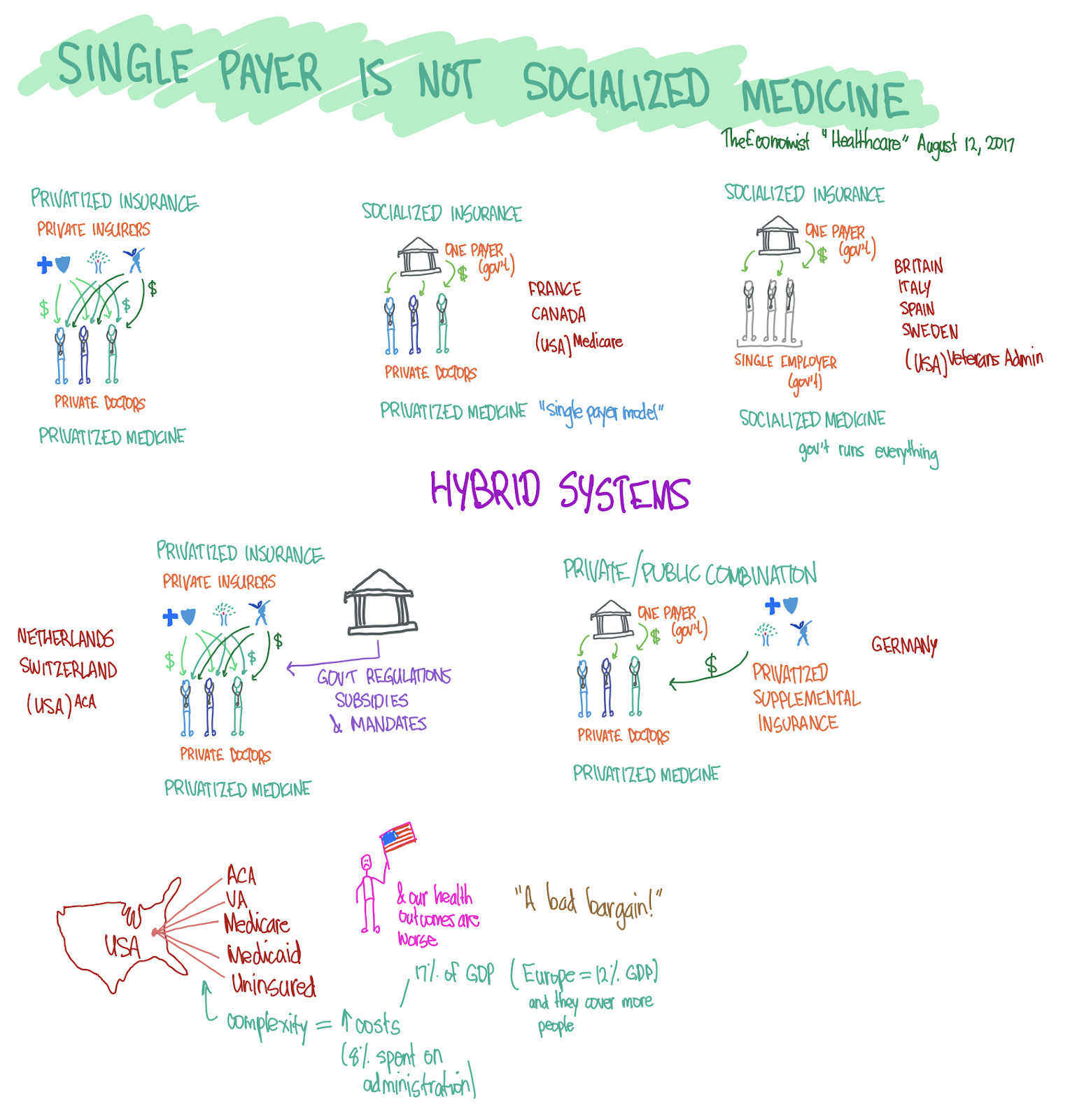

How do other countries do it?

Obviously, our system is not the only method around. There are other mixes of insurance and medicine delivery used around the globe. Below is a picture that shows the various ways we can mix and match public and private insurance with public and private providers. Also, regardless of what you think about the ACA, the common critique that the ACA is socialized medicine is not correct.